Insights

VAGO report into development contributions unveils the need for a root and branch review

Posted April 03, 2020

The Victorian Auditor General’s Office (VAGO) released its report on Managing Development Contributions on March 18, 2020. This is an audit report and not a policy review. Consequently, several important nuances and principles relevant to reform of the development contribution system in Victoria are not discussed. Nevertheless, the Auditor’s instincts are right on target. Development contributions in Victoria are a mess; a root and branch review is required.

VAGO audit report critical of current development contributions system

The VAGO audit covers the Growth Area Infrastructure Contribution (GAIC), Infrastructure Charges Plans (ICPs) and Development Contribution Plans (DCPs) provisions of the Planning and Environment Act plus ad hoc ‘voluntary’ contributions made under S173 of the Act.

The report is critical of both the design and administration of these arrangements. It finds that the responsible agencies – DELWP, VPA and the State Revenue Office - have “not managed these development contribution tools strategically to maximise their value and impact. Instead, they manage the tools in isolation, with overlapping roles and no overarching strategy, goals or plan to drive and measure their collective success”.

VAGO concluded that:

- Revenue collections under GAIC are unreliable due to deferred payment options built into this system

- The allocation process for GAIC funds is opaque and potentially inequitable across the growth areas

- The implementation of ICPs in growth areas has failed to deliver the clarity and administrative cost savings promised when these reforms were introduced in 2016

- The rollout of ICPs in major brownfield and regional growth areas has stalled, leaving many Councils without the funding tools they expected to apply in these areas

- While DCPs remain an option for many municipalities outside the growth areas, these plans remain costly and complex to prepare, and

- Councils have been given little support in finding and implementing the best development contribution mix for their areas.

VAGO’s is an audit report not a policy review. Consequently, several important nuances and principles relevant to reform of the development contribution system in Victoria are not ventilated.

The VAGO report treats all development contributions as simply ‘money for infrastructure to support growth’. However, the GAIC is a tax on the uplift in land value when land is brought from rural to urban uses, while ICPs and DCPs represent a form of user charge. Principles of nexus, fair apportionment and accountability vary across these domains.

The VAGO report is also partial in its scope. It does not address public open space contributions made under the Subdivision Act or Clause 53.01 of the Victoria Planning Provisions, nor does it consider Infrastructure Recovery Charges levied in certain areas under the Development Victoria Act.

Nevertheless, the Auditor’s instincts are right on target. Development contributions in Victoria are a mess; a root and branch review is required.

What is needed first is conceptual clarity about the different types of development contribution and how they could knit together into a simple, cohesive system that all stakeholders can understand.

VAGO report could trigger a modern contributions system

The VAGO report could be the trigger for a concerted, largely bi-partisan, effort to equip the State with a modern contributions system which is both friendly to business and more revenue effective for Councils and the State Government.

The starting point ought not be an administrative clean up, although that will be essential once we know where we want to take the system.

Rather what is needed first is conceptual clarity about the different types of development contribution and how they could knit together into a simple, cohesive system that all stakeholders can understand.

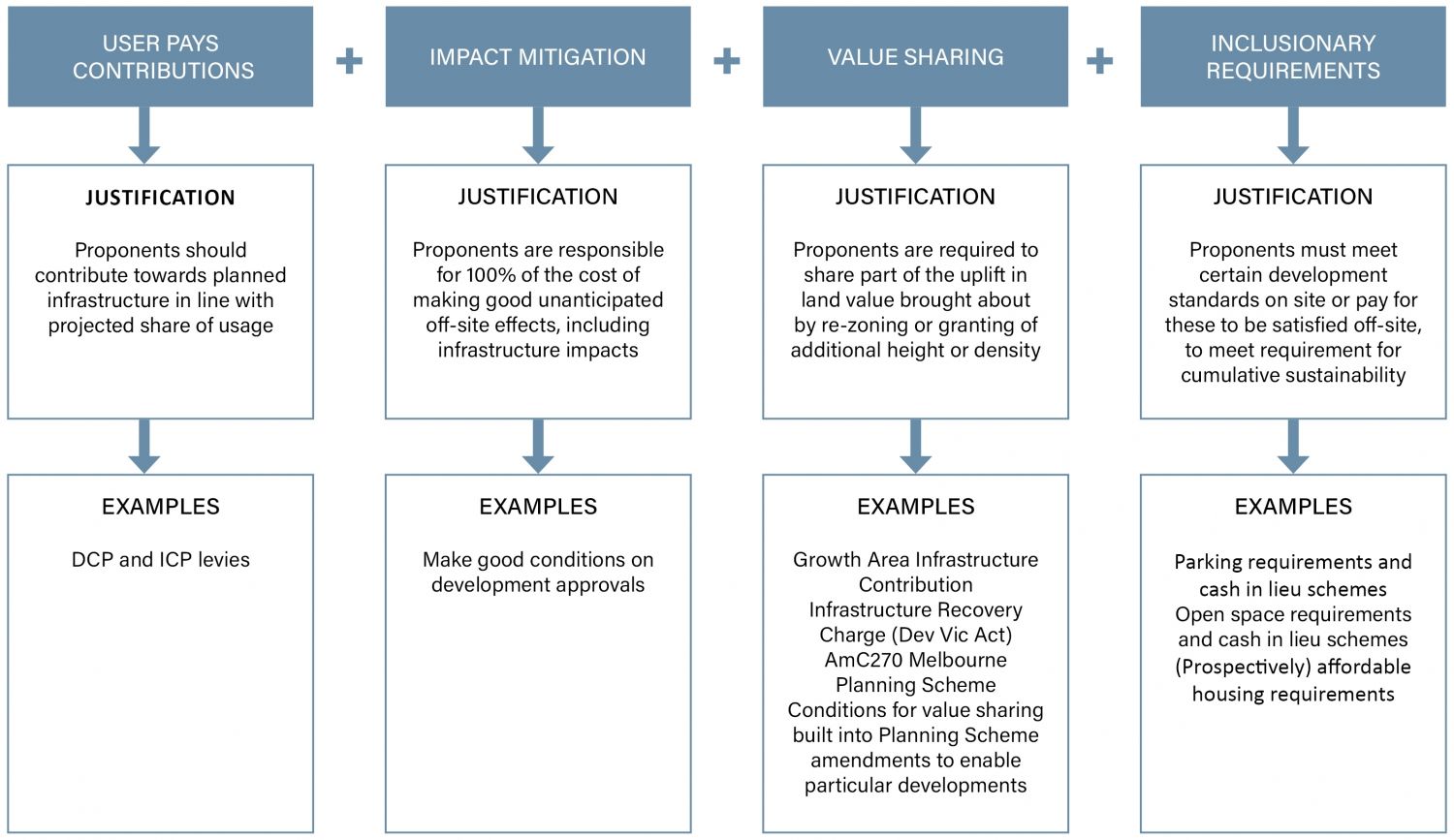

Any requirement for a development contribution will fall into one of four mutually exclusive and additive categories:

- user pays charges

- impact mitigation payments

- value sharing requirements, and

- inclusionary provisions.

Figure 1: Types of Development Contribution

User pays contributions

User pays contributions are collected via the ‘DCP’ and ‘ICP’ provisions of the Planning and Environment Act. Sometimes, they are applied outside these provisions via ad hoc negotiated agreements, or requirements set out in a Development Plan Overlay.

The user pays principle requires proponents to contribute cash or in-kind towards infrastructure benefitting their project, with the contributions linked to the proportion of usage of the infrastructure items in question.

Funds collected must be used for the delivery of the planned infrastructure or they must be returned to the current owners of the land which generated the user pays revenues. This is the accountability principle built into the DCP/ICP provisions of the Act.

Impact mitigation payments

Impact mitigation payments apply when developers are required to offset or compensate for the unanticipated adverse effects of their projects on the natural, built or social environment.

For example, if a development incorporates significantly more site coverage and would, therefore, result in stormwater runoff that exceeds the parameters which had been built into an area wide contribution scheme (DCP) for drainage, that particular proponent may reasonably be requested to meet 100 per cent of the cost of, say, an off-site retarding basin or tank to manage the additional flows.

This requirement is premised on the ‘exacerbater pays’ principle where the party responsible for the damage must meet the full cost of making it good, even though others may subsequently benefit from the off-site retention facility. This is clearly distinct from the ‘user pays’ principle where, as noted, costs are shared according to projected share of usage.

Value sharing requirements

Value sharing requirements, like the GAIC, are premised on another, separate and distinct, principle relating to the efficient regulation of community sanctioned development rights.

The State deliberately and systematically rations access to ‘development rights’ via planning regulations. Governments apply this rationing because it is expected to generate a net community benefit compared to allowing urban development to proceed on a laissez-faire basis.

The value of regulated development rights is capitalized into the price of land. For example, other things equal, a piece of land which is enabled for use as a major shopping centre will be more valuable than land without this privileged access to retail centre development rights. Similarly, land enabled for a multi-storey apartment building will be worth more than otherwise equivalent land designated for a single household dwelling, and so on.

As occurs with other regulated markets, for example, commercial fisheries, mineral exploitation, broadcasting bandwidth and so on, it is appropriate to charge a licence fee for access to these regulated development rights.

Inclusionary provisions

Inclusionary provisions are premised on minimum acceptable standards of development with the proponent sometimes having the option to fulfil the required performance standard off-site through a cash or in-kind contribution.

Cash-in-lieu schemes have been operated for the fulfilment of car parking requirements for decades and are now formalised in the Victorian Planning Provisions (VPP). Cash payments in lieu of provision of 5 per cent (or more) of land for public open space upon approval of subdivision is another example of the ‘inclusionary standards’ premise for requiring cash or in-kind contributions from a development proponent.

Given their different public policy justifications, a ‘one size fits all’ approach to the design and administration of these four development contribution types could easily have perverse outcomes. For example, if the user pays principle is watered down in the first category of contributions, and there is no impact mitigation system, developers will face weakened price signals to focus on areas where the cost of extending infrastructure is lower. Left unchecked, this will fuel more sprawl and out of sequence development.

But while each category of contribution requires its own policy design, cognizant of the fit with other categories, this does not mean that the contribution regime has to be complex. There is scope for rapid and wholesale simplification.

Two keystone reforms

Improve DCP/ICP system

The DCP / ICP system can be improved by supporting Councils to adopt whole of municipality contribution plans rather than a patchwork of precinct or site specific plans which characterises the system at present.

This would see off the duplication of strategic planning effort that goes into preparing multiple plans, saving literally millions of dollars across the system. It would also deal with the obvious equity problem of charging developers in some parts of a municipality an infrastructure fee while others get away scot-free.

The effort and know-how required to prepare a whole of municipality DCP is comparable to those employed in creating a Council’s annual budget. It can be readily mastered by local government officials, especially given the range of custom software now available to support the process*.

A large part of the ‘unreasonable cost’ of putting together a DCP, to use VAGO’s language, relates to the torturous process of amending a planning scheme, including a potentially litigious panel hearing.

DCPs are essentially technical documents. While rigorous scrutiny is undoubtedly required, the matters likely to be in dispute are amenable to resolution against objective standards; they typically do not require policy judgements as such. The same distinction exists in assessing compliance in building permit applications versus appraisal of policy alignment in planning permit applications.

A dedicated team in the Essential Service Commission could scrutinise proposed DCP charges for compliance with the fairness and efficiency principles in the Act and recommend (or otherwise) approval via a fast track amendment process. This already occurs in other jurisdictions, notably in NSW and Queensland.

Recast the GAIC as universal licence fee

A second strategic reform would see GAIC abolished and replaced with a universal development licence fee. Again this would resolve a glaring equity issue – the State insists on value sharing in greenfield development under current arrangements, but land owners in brownfield, infill and regional areas capture 100% of the uplift in land value associated with rezonings and discretionary development approvals.

A universal development licence fee can operate on a pre-scheduled or ‘codified’ basis rather than relying on before and after valuations of sites subject to planning related uplift. Such a system operates in the ACT.

Provided enough of the uplift is ‘left on the table’ to motivate land owners to release their sites to bona fide developers, the licence fee would be non-distortive and would generate new revenue quite likely calculated in the hundreds of millions per year. If, in turn, this revenue were shared with local governments, not only would there be a significant boost for infrastructure investment, Councils may even become more welcoming of densification, thereby providing more opportunities for the development sector.

*SGS has developed a cloud based tool, ShapeVIC, for both the formulation of DCPs and the ongoing monitoring of transactions once these Plans are in force.

Connect with us on LinkedIn